Creating a budget is the foundation of financial stability. Whether you want to pay off debt, save for a goal, or simply stop living paycheck to paycheck, a well-crafted budget puts you in control of your money. This guide will walk you step-by-step through creating your first budget successfully.

Why Do You Need a Budget?

A budget is not about restriction. It’s a tool to help you:

- Understand where your money goes

- Avoid overspending

- Save for emergencies and goals

- Reduce financial stress

- Plan for the future

Step 1: Calculate Your Total Income

What Counts as Income?

- Full-time or part-time job salaries (after taxes)

- Freelance or side gig earnings

- Passive income (rent, dividends, royalties)

- Government benefits or child support

👉 Use your average monthly income if your earnings fluctuate.

Step 2: List All Your Expenses

Break your expenses into two main categories:

Fixed Expenses (same every month)

- Rent or mortgage

- Utilities

- Insurance

- Car payments

- Subscriptions (Netflix, Spotify, etc.)

Variable Expenses (change monthly)

- Groceries

- Dining out

- Gas/transportation

- Entertainment

- Shopping

Periodic Expenses

- Annual insurance payments

- Car maintenance

- Gifts/holidays

👉 Tip: Review your bank statements from the last 2–3 months to catch everything.

Step 3: Categorize Your Expenses

Group your spending into manageable categories:

- Needs: housing, utilities, groceries, insurance

- Wants: dining out, entertainment, hobbies

- Savings/Debt Payments: emergency fund, investments, extra debt payments

Step 4: Choose a Budgeting Method

Popular Methods:

- 50/30/20 Rule:

- 50% Needs

- 30% Wants

- 20% Savings/Debt Repayment

- Zero-Based Budget:

- Every dollar has a job.

- Income – Expenses = 0 at the end of the month.

- Envelope System (Cash Budgeting):

- Assign cash to different categories.

- Spend only what’s in each envelope.

Choose the one that fits your lifestyle best.

Step 5: Set Financial Goals

A budget should reflect your goals.

Examples:

- Build an emergency fund

- Pay off $5,000 in credit card debt

- Save $3,000 for a vacation

- Invest 10% of your income

Set SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound.

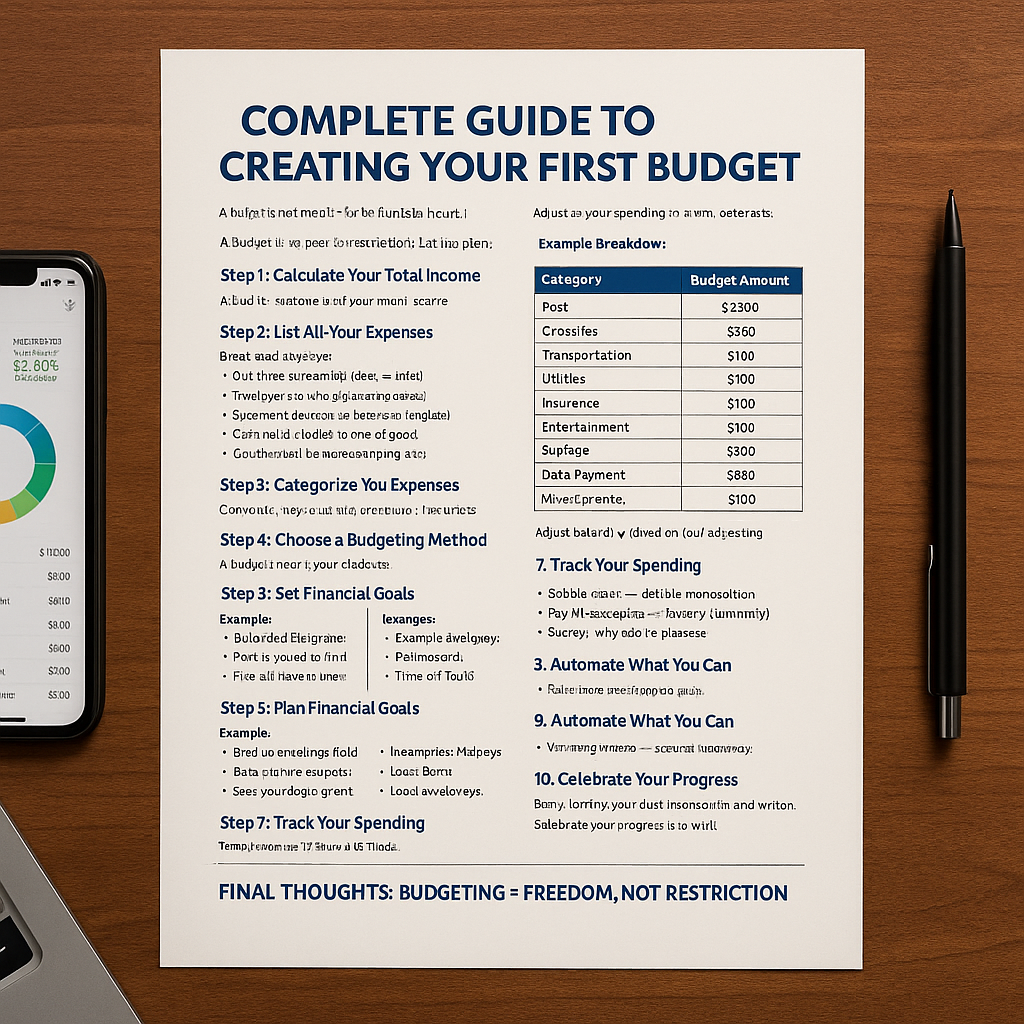

Step 6: Plan Your Monthly Budget

Example Breakdown:

| Category | Budget Amount |

|---|---|

| Rent | $1,200 |

| Groceries | $400 |

| Transportation | $150 |

| Utilities | $100 |

| Insurance | $100 |

| Entertainment | $100 |

| Savings | $300 |

| Debt Payment | $250 |

| Miscellaneous | $100 |

Adjust based on your income and priorities.

Step 7: Track Your Spending

Tools to Use:

- Apps: Mint, YNAB, Goodbudget, PocketGuard

- Spreadsheets (Google Sheets, Excel)

- Pen and paper notebook

Track daily or weekly to avoid surprises at the end of the month.

Step 8: Review and Adjust

Budgets are living documents. Each month:

- Review your spending

- Adjust categories as needed

- Look for areas to cut back

- Add more to savings or debt payoff when possible

Step 9: Automate What You Can

Set up:

- Automatic bill payments

- Automatic transfers to savings or investment accounts

Automation reduces stress and ensures consistency.

Step 10: Celebrate Your Progress

Every month you stick to your budget is a win. Celebrate by:

- Treating yourself (within budget)

- Watching your savings grow

- Seeing your debt shrink

Final Thoughts: Budgeting = Freedom, Not Restriction

A budget is a plan for your money, not a punishment. When you control your money, you control your future. Whether your goal is to get out of debt, travel, buy a home, or retire early, it all starts with a budget. The first one may feel imperfect — that’s okay. Keep adjusting, learning, and moving forward.